In 2014, the Federal Reserve Bank of Philadelphia published a report that showed a high incidence of use of prepaid debit cards1 by millennials. And it revealed that many perceptions about prepaid cards just didn’t hold water, at least not among this age group.

Prepaid cards have evolved over the years. New prepaid cards have entered the market, and a number have exited. Today’s prepaid debit cards tend to offer more features and have lower fees.

So, we conducted a survey2 of millennials3 that focused just on prepaid card users to test current views of prepaid cards and how millennials are using the cards.

The survey covers four primary areas:

- Use of other financial products among millennial prepaid card users

- How millennials use their prepaid cards

- How millennials select and purchase prepaid cards, and

- Millennials’ view of their prepaid cards and their fees

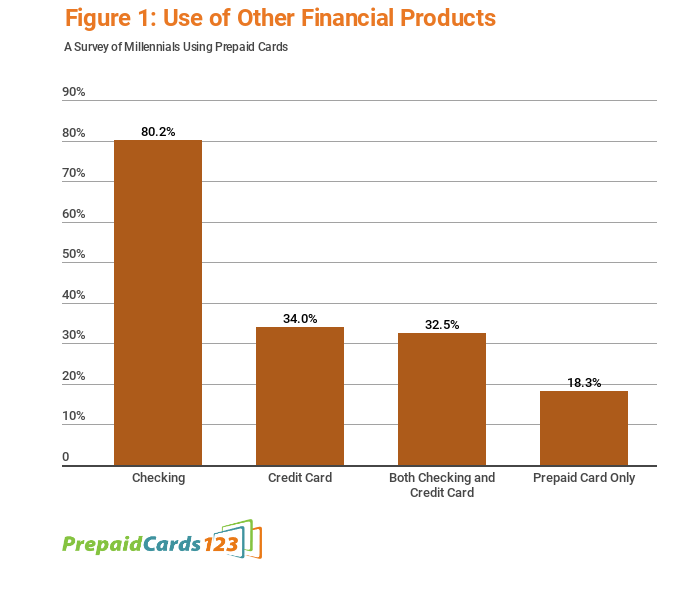

Use of Other Financial Products

Millennials that use prepaid debit cards, by and large, are not using them exclusively.

Over 80% have a checking account in addition to their prepaid card. Thirty-four percent have a credit card. Only 18% said they had neither a checking account nor a credit card.

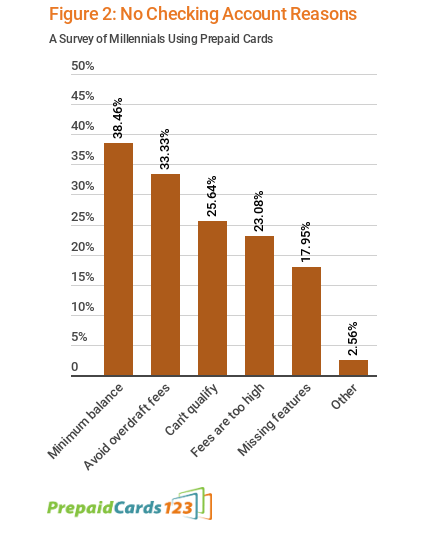

Among the 20% that do not have checking accounts, only 27% reported not having a checking account because they believe they were unable to qualify for one. Those without checking were more concerned about not wanting to maintain a minimum balance (38%) and wanting to avoid overdraft fees (33%).

Prepaid debit cards can help users avoid overdraft fees, and they don’t require a minimum balance. However, for checking accounts that require a minimum balance, the requirement is generally to avoid a monthly fee. Yet only 23% cited fees as a reason for not having a checking account. The absence of needed features was the least common reason (18%).

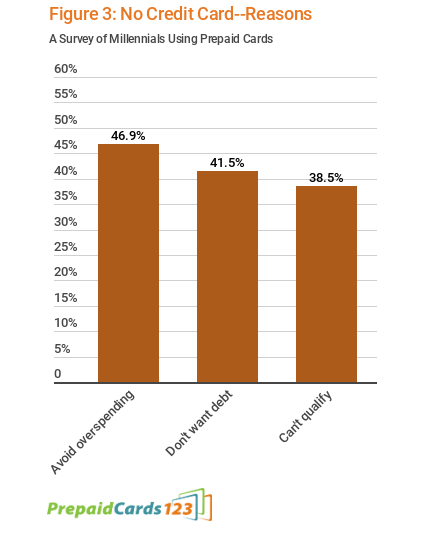

As with checking accounts, more prepaid card users without a credit card said they did not have one by choice than the inability to qualify for one. Forty-seven percent said they did not want to spend more than they have, and 42% said they want to avoid the debt. Only thirty-nine percent said they do not have a credit card because they are unable to qualify for one.

Respondents were asked “If you don’t have a credit card, which reasons describe why?” Respondents could select multiple responses from the following:

- I don’t think I can qualify

- I don’t want to have debt

- I don’t want to spend more than I have

or respondents could choose the response “I have a credit card. None of these apply.”

How Millennials Use Prepaid Debit Cards

Prepaid debit cards carry one of the major network brands–Visa, Mastercard, American Express, or Discover. Cardholders can use the cards for purchases like credit cards issued through those same payment networks and get cash with the cards like checking account debit cards. But they’re not associated with a bank account. So users must add value to the cards when they deplete the funds on the card.

Survey respondents were asked about their use of their prepaid cards for spending, cash access, and adding money.

Spending

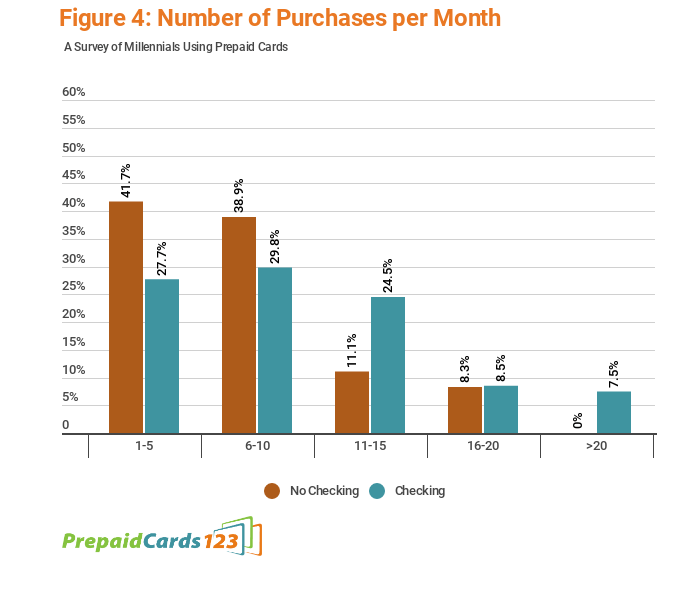

Not surprisingly, almost all respondents–over 98%–use their prepaid cards to make purchases. Somewhat more surprising, however, is that those with other spending options made more frequent purchases using their prepaid cards.

While the majority of card users made 10 or fewer purchases per month using their card, forty percent of prepaid card users with checking and 39% of users with both a checking account and credit card made 11 or more purchases per month with their prepaid card. Only 19% of users without a checking account made 11 or more purchases per month.

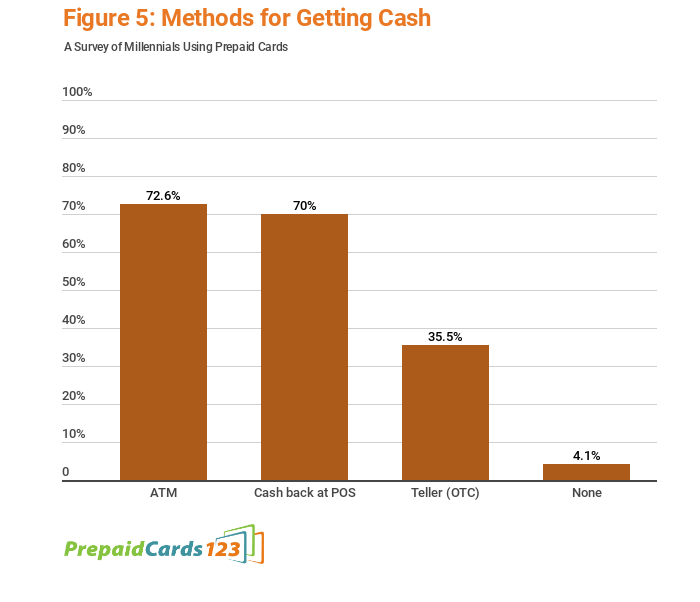

Getting Cash

Nearly all prepaid debit cards provide three ways to get cash from the card:

- ATM withdrawals

- Cash back when making a debit purchase

- Over-the-counter withdrawals

Most millennials use both ATM and cash back at the point-of-sale to access cash from their prepaid cards.

ATM Use

Prepaid card users can access cash at any ATM that carries their payment network’s logo. They can get cash back when making a debit purchase at retailers, like grocery stores, convenience stores, and big box home improvement stores. Cash back at the point of sale is also available at other services locations like the post office. Prepaid card users can get cash using over-the-counter withdrawals at bank tellers and some other financial service locations.

Fees vary significantly among prepaid cards for cash access. A little less than half of prepaid cards currently offer a free ATM network.4 Like bank account debit cards, all prepaid cards a fee for out-of-network withdrawals, ranging from $1.00 to $3.00 per withdrawal, with an average of $2.24.

The fees are similar to fees charged by major banks for out-of-network ATM use.5 However, banks offer free ATM withdrawals at ATMs owned by the bank and often an ATM network beyond their own ATMs.

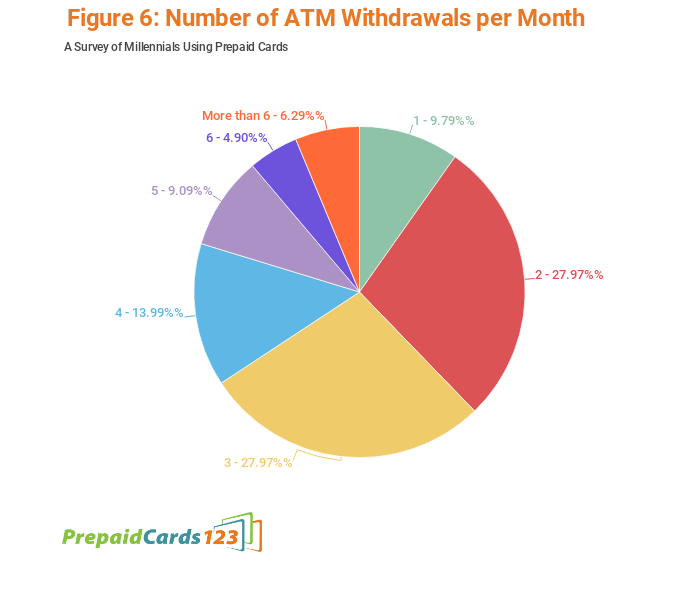

Despite the fees, millennials use their prepaid cards at ATMs regularly for cash withdrawals. Seventy-three percent of prepaid card users get cash at ATMs using their cards. Nearly half of respondents use their prepaid card for three or more ATM withdrawals per month. Those with checking accounts used their prepaid card at the ATM as much or more than those without.

Cash Back at Point of Sale

The vast majority of prepaid cards do not charge a fee to get cash back when making a debit purchase, although a minority of cards charge a transaction fee for the purchase itself. While also a highly used method to get cash, getting cash back at the register is used slightly less than ATMs (72%). Those that get cash back at the register also use ATMs.

Over-the-Counter Withdrawals

Over-the-counter withdrawals can be the most expensive way to access cash from a prepaid card. Although prepaid cards issued by brick-and-mortar banks typically offer free over-the-counter withdrawals, most other cards charge the same fee that they charge for an out-of-network ATM withdrawal. Some charge significantly more–as high as $35.00. Over-the-counter withdrawals are also less convenient than ATMs and cash back at the register.

Only 33% of millennials get cash from over-the-counter withdrawals.

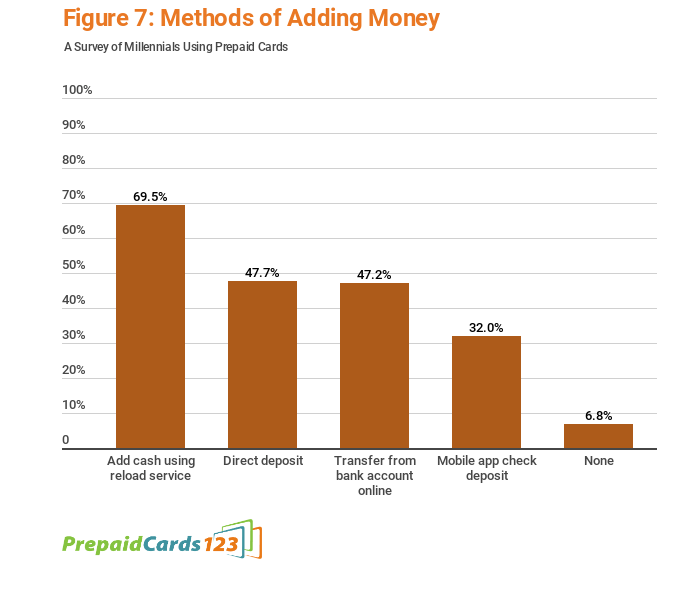

Adding Money

Nearly all prepaid cards offer two fee-free ways to add money to the card–direct deposit and bank account transfer.

Many prepaid cards also offer free check deposits through their mobile app. However, free check deposits require up to 10 days to have access to the funds. Expedited availability comes with a fee. Brick-and-mortar banks issuing prepaid cards often provide additional check deposit options, such as ATM and teller deposits.

In general, the most expensive option to add money to a prepaid card is adding cash. Although most card issuers don’t charge a fee, third-party cash reload services do. Fees range from $2.00 to $5.95.

Millennials are using the range of methods to add money to their prepaid cards. A substantial number use direct deposit (48%) and bank transfers (47%).

But despite the fees, more millennials load cash than any other method of adding money to their prepaid cards–70%.

“Which of these ways to add money to (or “load”) your prepaid debit card do you use?”

- I use direct deposit (of my paycheck or a benefit check)

- I deposit checks to my prepaid card using a mobile app

- I transfer money from my bank account online

- None of the above

“Do you add cash to your prepaid card using a reload service (e.g. Green Dot MoneyPak, Walmart Rapid Reload)?”

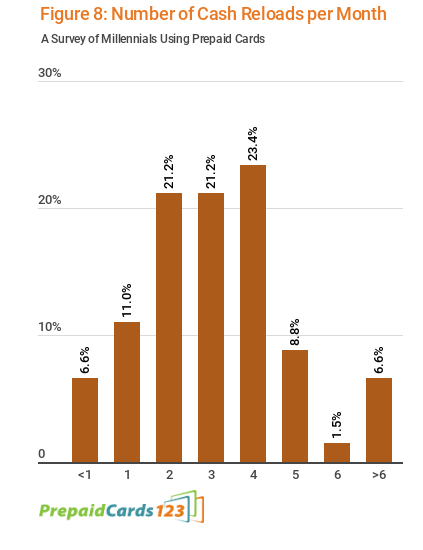

Among those that load cash through a reload service, 61% are loading cash 3 or more times per month.

Millennials’ Selection Among Prepaid Cards

There are currently over 60 prepaid cards on the market. Survey respondents were asked about where they purchased their prepaid card and how they selected their cards.

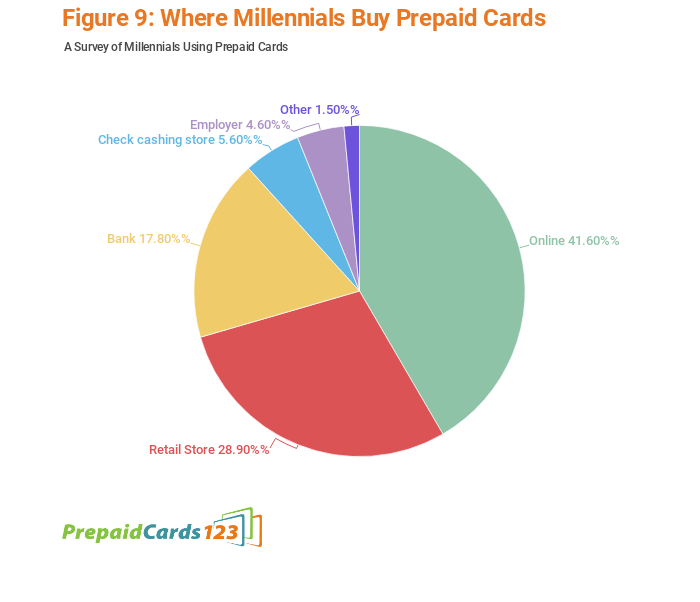

Where Millennials Get their Prepaid Cards

Nearly all prepaid cards can be obtained online. Many of the larger brand prepaid cards are available in retail stores like Walmart, Walgreens, CVS and convenience stores. They are also available in check cashing/payday lender locations.

Some brick-and-mortar banks issue prepaid cards only at their branch locations. Most, however, offer them online as well.

For cards offered in stores, the store often charges a purchase fee that can range from $1 to $4.95 or more. Most card issuers, however, do not charge a fee to purchase the card online.

For cards purchased online, it takes 7-10 days to receive the card. Cards purchased in stores can be loaded when purchased and used immediately to make purchases. But ultimately, cards purchased in stores must be activated online to reload the card or use most other functions, such as direct deposit or web/mobile account access.

Forty-two percent of millennials are opting for the cheaper option, purchasing their cards online. Twenty-nine percent purchased their cards in stores. Eighteen percent got their cards at a bank. Only 6% reported buying their cards at payday lenders.

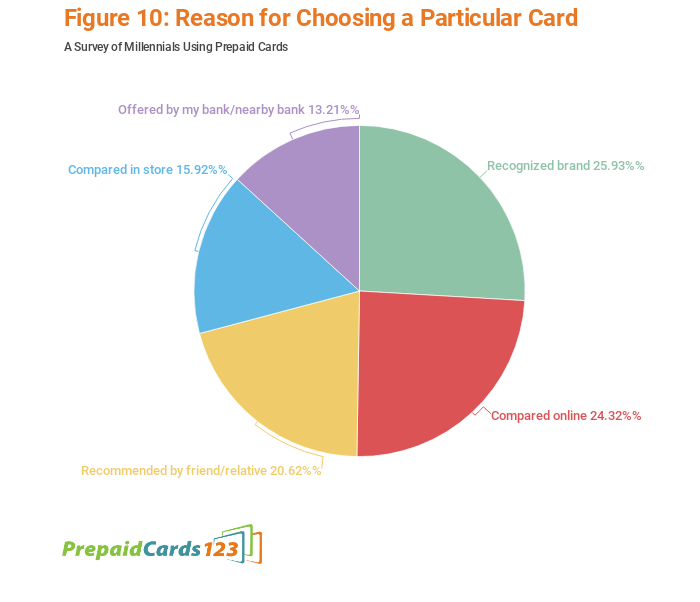

Brand Recognition and Online Comparison Influences Millennials’ Selection

Thirty-eight percent of respondents said their comparison of prepaid cards, either online (23%) or in stores (15%), dictated their choice among cards. But brand recognition was more common than either (25%).

Only 13% chose a card because it was offered by their bank or a bank close to them. Nineteen percent relied on a recommendation by a friend or family member.

Respondents were asked “Which of the following best describes how you chose your prepaid debit card?” Respondents could choose a single selection from:

- My prepaid card was recommended by a friend or family member

- I compared prepaid cards online

- I compared prepaid cards in the store

- My prepaid card was offered by my bank or a bank close to me

- I recognized my prepaid card’s brand

- It was given to me by someone else (e.g. my employer), so I didn’t have a choice

Five respondents that chose the last response, indicating they did not choose, were excluded from the results.

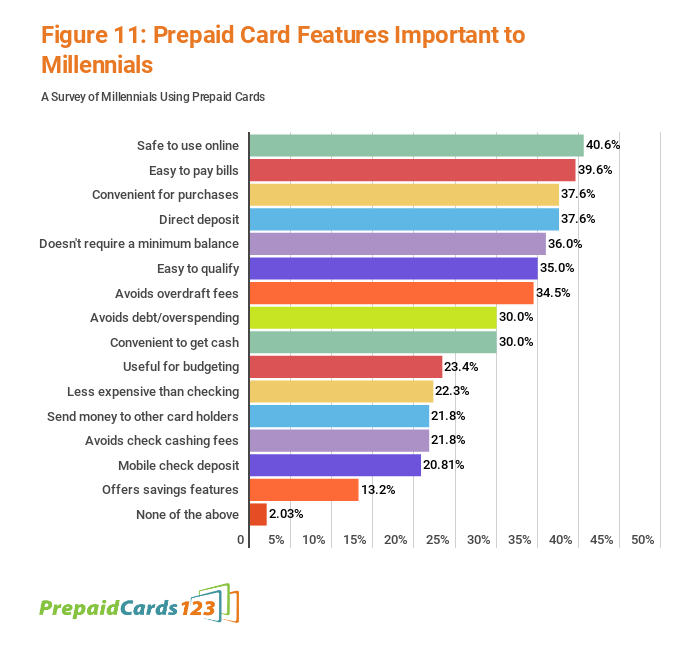

Important Features

All prepaid cards share some of the same functions. They can be used to separate money from a checking account for a specific category or type of spending. They can be used to avoid checking overdraft fees. And they can be used as a credit card alternative to avoid incurring debt.

But prepaid cards have evolved to offer more features beyond spending and avoiding bank fees or debt. Most cards now offer mobile apps that can be used to check balances and make check deposits. Some prepaid cards offer bank-like bill pay services, and a few cards even offer more sophisticated budgeting features to set limits on spending categories or interest-bearing savings accounts.

The survey respondents were asked to identify from a list of features which ones were important to them. No single feature was chosen by a majority of card users.

The features deemed important by the most users were online safety (41%), easy to pay bills (40%), and convenience in making purchases (38%).

Features that are important to the fewest are a savings component (13%) and mobile check deposits (21%).

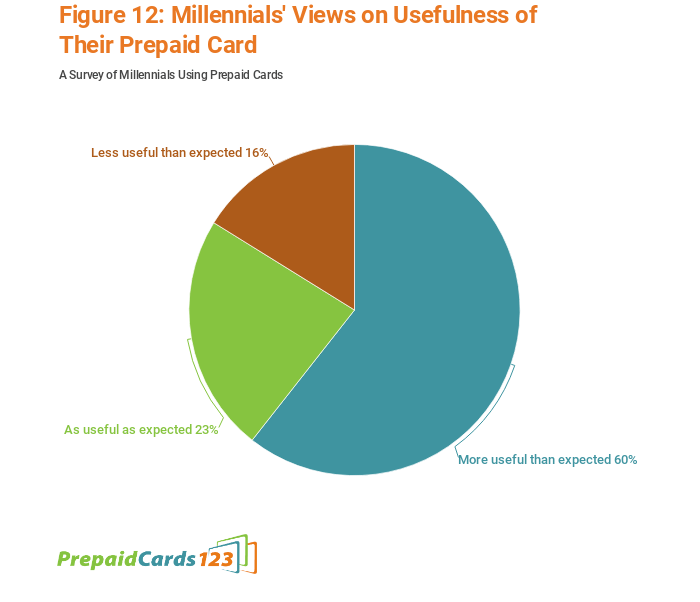

Prepaid Cards Meet or Exceed Millennials’ Expectations–Even the Fees

While the features that millennials deem important vary, one thing is true for the majority. They are happy with their prepaid cards.

When asked to rate their experience with their prepaid card, over 60% of respondents described their cards as “more useful than expected.” Twenty-three percent said it met their expectations. Only 16% described their cards as less useful than expected.

Respondents were asked to make a single selection in response to “Which of these statements describes your experience with your prepaid debit card?”

- My prepaid card is less useful than I expected

- My prepaid card is more useful than I expected

- My prepaid card is about as useful as I expected

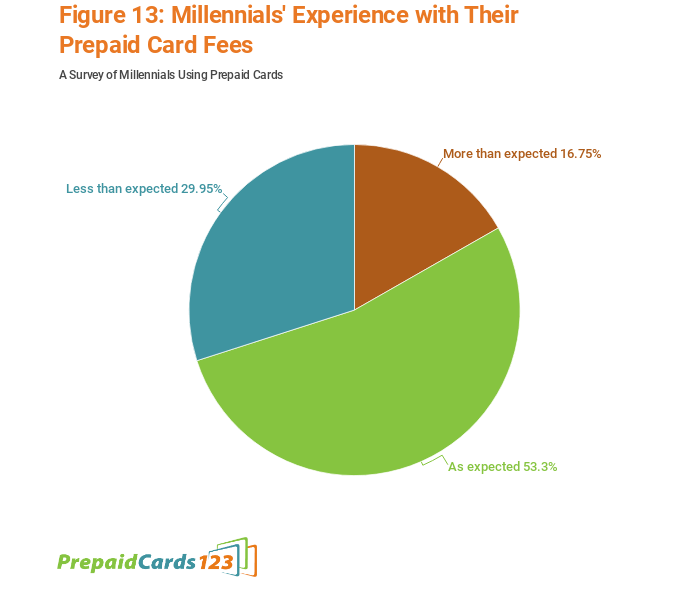

Even when asked about fees, over 80% said that their card’s fees met expectations (53%) or were lower than expected (30%). Only 17% said fees were higher than anticipated.

Respondents were asked to make a single selection in response to “Which of these statements describes your prepaid debit card’s fees?”

- The fees are less than expected

- The fees are about what I expected

- The fees are more than what I expected

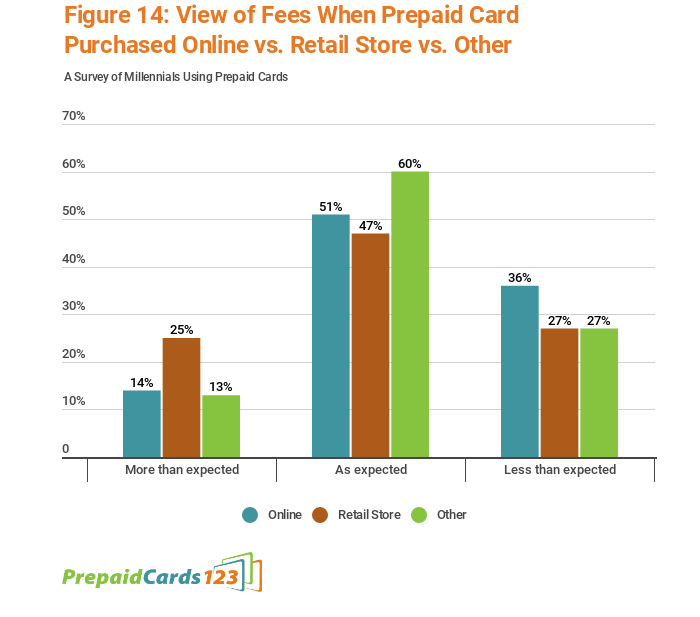

Notably, those that were surprised by their card’s fees increased to 25% for respondents that purchased their cards in retail stores. Still, 47% of that group said fees met expectations and 27% said fees were less than expected.

Some Takeaways

Prepaid cards used to be characterized as a replacement for a checking account for those that did not want or could not get a traditional bank account. Clearly, that is no longer the case, at least among millennials. While prepaid cards still serve that purpose for some, the majority are using the cards alongside a checking account.

And fees, or at least fees alone, are not dictating how millennials use their accounts. Millennials are conducting fee-based transactions with their prepaid cards when fee-free alternatives are available to them, such as ATM withdrawals from prepaid cards when no-fee ATMs are available with their checking accounts and when free POS cash back transactions are available with the cards themselves. The same is true for cash deposits for those with checking accounts.

Even with the likely additional cost, millennials are not using their prepaid cards’ services begrudgingly. The vast majority say prepaid cards met or exceeded their expectations on fees. In some respects, that comports with the federal reserve’s observations in its 2015 update6 to its broader survey of millennials’ use of alternative financial services beyond just prepaid cards.

They have [checking accounts] but also use prepaid cards and check cashing services. They have credit cards but also use payday loans and pawn shops. Their preferred banking channel is the Internet, but they also use branches.

Millennials have and use multiple financial options and those options often have overlapping functions. One can argue that there are better options, at least less costly ones, for some of the ways millennials are using prepaid cards. But perhaps choice itself has utility among this age group. In any event, the survey demonstrates that however millennials choose and use prepaid cards, they’re happy with that choice.

Notes

1. Millennials with Money: A New Look at Who Uses GPR Prepaid Cards, Susan Herbst-Murphy and Greg Weed (September 2014). For purposes of this article, “prepaid debit cards” and “prepaid cards” refer to general purpose reloadable prepaid cards. The Federal Reserve has used the term “general purpose” to describe prepaid cards that are branded with one of the major payment networks as opposed to store-branded charge cards. “Reloadable” refers to prepaid cards that allow depositing money to the cards after the initial funds are depleted, as opposed to gift cards that cannot be added to after the initial purchase.

2. The survey questions were created by B&C Media, LLC. The survey was distributed by Pollfish to mobile device users that have opted into its survey service. Six hundred ninety respondents answered an initial screening question to determine if they were current prepaid card users. Two hundred users were qualified to respond to the remainder of the survey. Three respondents identified an online checking account debit card as a prepaid card and were excluded. Survey results presented represent the remaining 197 respondents.

3. For purposes of the survey, “millennials” refers to those born from 1981 to 1996.

4. We reviewed 41 prepaid cards. Twenty offer a free ATM network. The average out-of-network fee charged by the prepaid card is $2.24.

5. ATM Fees: How Much Does My Bank Charge?, GOBankingRates.com (Jan 2018).

6. Millennials with Money Revisited: Updates from the 2014 Consumer Payments Monitor, Susan Herbst-Murphy and Greg Weed (December 2015).